This new S&P 500 entrant is up 50% in 2026; Time to buy?

March 08, 2026

Vertiv Holdings (NYSE: VRT), a provider of critical digital infrastructure for data centers, has surged this year amid booming demand for AI-related power and cooling solutions.

Indeed, the stock’s momentum comes amid growing fundamentals, making the equity a possible buy for investors.

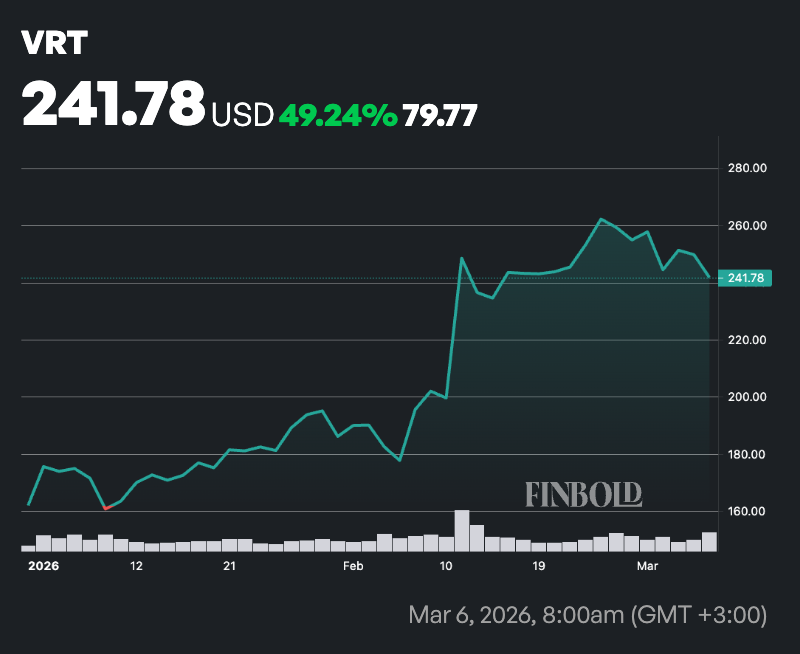

As of press time, VRT stock was trading at $241, reflecting a year-to-date gain of approximately 49% from its 2025 year-end level.

The stock is also seeing renewed momentum after it was announced that Vertiv will join the S&P 500 index, effective before the opening of trading on March 23, as part of the quarterly rebalance.

The addition also includes Lumentum Holdings, Coherent, and EchoStar.

Notably, index inclusion is expected to drive increased visibility and potential inflows from passive funds tracking the benchmark.

Vertiv fundamentals

Several factors position Vertiv as a compelling buy for growth-oriented investors. Foremost is its strategic exposure to the AI data center ecosystem, where it dominates in power management, liquid cooling, and thermal solutions essential for hyperscale computing.

Partnerships with industry leaders like Nvidia (NASDAQ: NVDA) and recent collaborations with Generate Capital and Hut 8 point to its role in scaling AI deployments.

At the same time, the company’s fourth-quarter 2025 results were exceptional, with net sales up 23% year over year, organic orders surging 252%, and a record backlog of $15 billion providing strong revenue visibility into 2026 and beyond.

Guidance for 2026 projects revenue of $13.25 billion to $13.75 billion, implying 27% to 29% organic growth, and adjusted EPS growth of about 43% at the midpoint.

Additionally, Vertiv’s upcoming inclusion in the S&P 500 index is expected to enhance liquidity, attract passive fund inflows, and increase institutional interest.

VRT stock risks

Despite these strengths, several risks could temper enthusiasm and potentially pressure the stock price. Valuation is a primary concern, with a trailing price-to-earnings ratio of 70 to 74 times and a forward P/E in the mid-30s to mid-40s, significantly above peer averages in the electrical equipment sector and the broader U.S. market.

Meanwhile, Vertiv’s heavy reliance on AI and hyperscaler capex cycles introduces cyclical risk; any moderation in data center buildouts could impact order growth and backlog conversion.

Execution challenges, such as supply chain disruptions, capacity ramp-ups, or delays in new facilities, pose threats to meeting guidance. Competition in the data center infrastructure space is intensifying, with peers potentially eroding market share.

Meanwhile, insider selling, including a recent $51 million disposal by an independent director, may signal caution at current levels.

The stock’s high beta amplifies volatility, as seen in recent swings tied to AI market sentiment, while broader risks such as interest rate changes or energy policy shifts affecting data center power demand could also weigh on the stock.

Featured image via Shutterstock